UK FinTech Shines Bright Amid

The Covid Gloom

M&A

(Cancelled)

SPAC

VC

“The industry is starting to mature but the wider opportunity remains nascent where incumbents still dominate in terms of market share”

– Tim Levene, Augmentum FinTech

Weathering the Storm

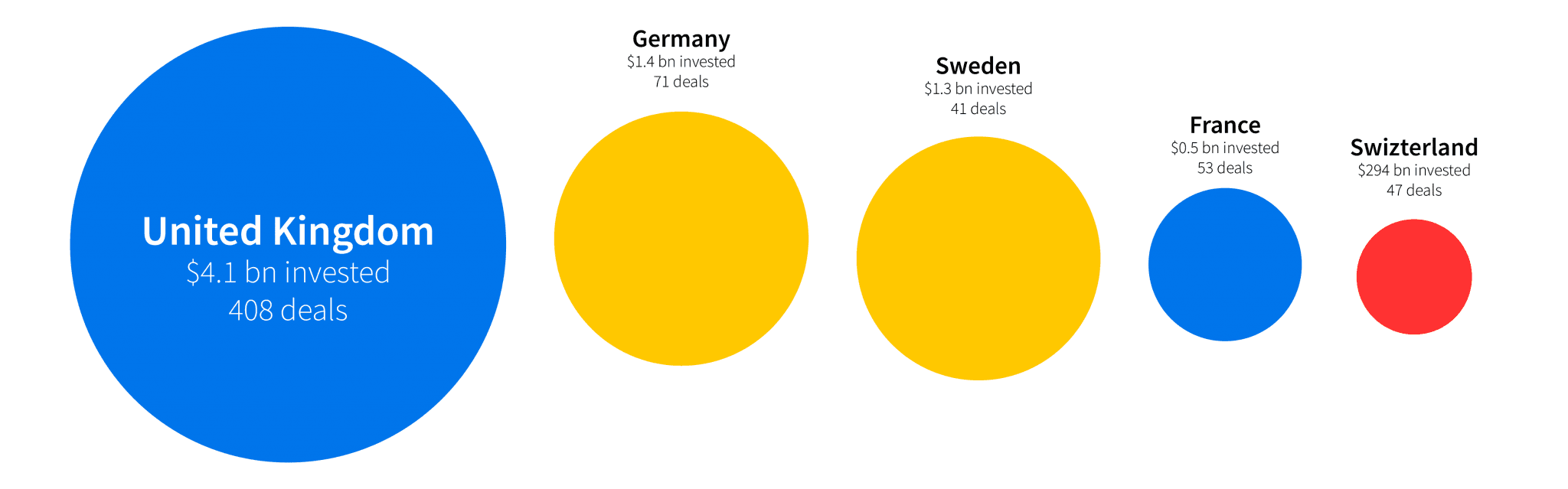

European Top 5 Countries by Investment

“The global investment community recognises the UK as one of very few places that combines world-leading technical talent with a deep pool of FinTech entrepreneurs who, having had venture capital experience previously, know how to build at the velocity and scale that is required”

– Kevin Chong, Co-Head, Outward VC

More mega-deals as UK FinTech matures

FinTech companies are continuing to grow and attract large investment rounds, as sign of the sectors maturity that we started to witness last year. Since the start of 2020, nine companies in the UK have closed mega-rounds (deals exceeding $100m).

“The UK fintech ecosystem has seen increasing interest from established overseas investors who are becoming more active not only in capital but by hiring local teams on the ground – a trend which has persisted in the first 3 weeks of 2021”

– Tim Levene, Augmentum Capital

- Revolut ($580m) was led by US investor TCV

- Checkout.com ($150m Series B and $450m Series C) was led by US investors Coatue and Tiger Global respectively

- Molo ($343m) was led by German investor Yabeo

- Rapyd ($300m) by US investor Coatue

- Onfido ($100m) by US investor TPG Growth

Company:

Deal Size:

Lead Investor:

Investor HQ:

$580m

TCV

USA

$150m (Series B)

$450m (Series C)

Coatue (Series A)

Tiger Global (Series B)

USA

$343m

Yabeo

Germany

$300m

Coatue

USA

$180m

Sprints Capital, Eurazeo, Wellington Management

Various

$166m

Accel, General Catalyst, Various Others

Various

$125m

Draper Esprit, British Patient Capital, Eurazeo

UK / EU

$123m

Merian Chrysalis, Harold McPike

UK / Bahamas

$100m

TPG

USA

Crystal Ball Gazing into 2021

Did you know that around 12% of the adult population in the UK – some six million people – downloaded their bank’s App for the first time during the first lockdown?

– Source: Nucoro report, April 2020